Introduction: Overview of the Insurance Industry in Bangladesh

Examining Bangladesh’s Insurance Industry reveals a sector that has witnessed remarkable transformation over the past few decades. As one of South Asia’s emerging economies, Bangladesh has experienced steady growth in its insurance market, reflecting the country’s broader economic development and increasing financial sophistication. The insurance industry plays a vital role in risk management, financial protection, and capital formation, contributing to the nation’s economic stability and growth trajectory.

The insurance sector in Bangladesh operates through a dual structure comprising life and non-life insurance segments, with both public and private entities participating in the market. Despite its potential, the industry faces unique challenges including low penetration rates, limited public awareness, and regulatory complexities. Understanding the nuances of this sector is essential for stakeholders, policymakers, and investors looking to engage with Bangladesh’s evolving financial landscape.

Regulatory Framework and Role of Insurance Development & Regulatory Authority

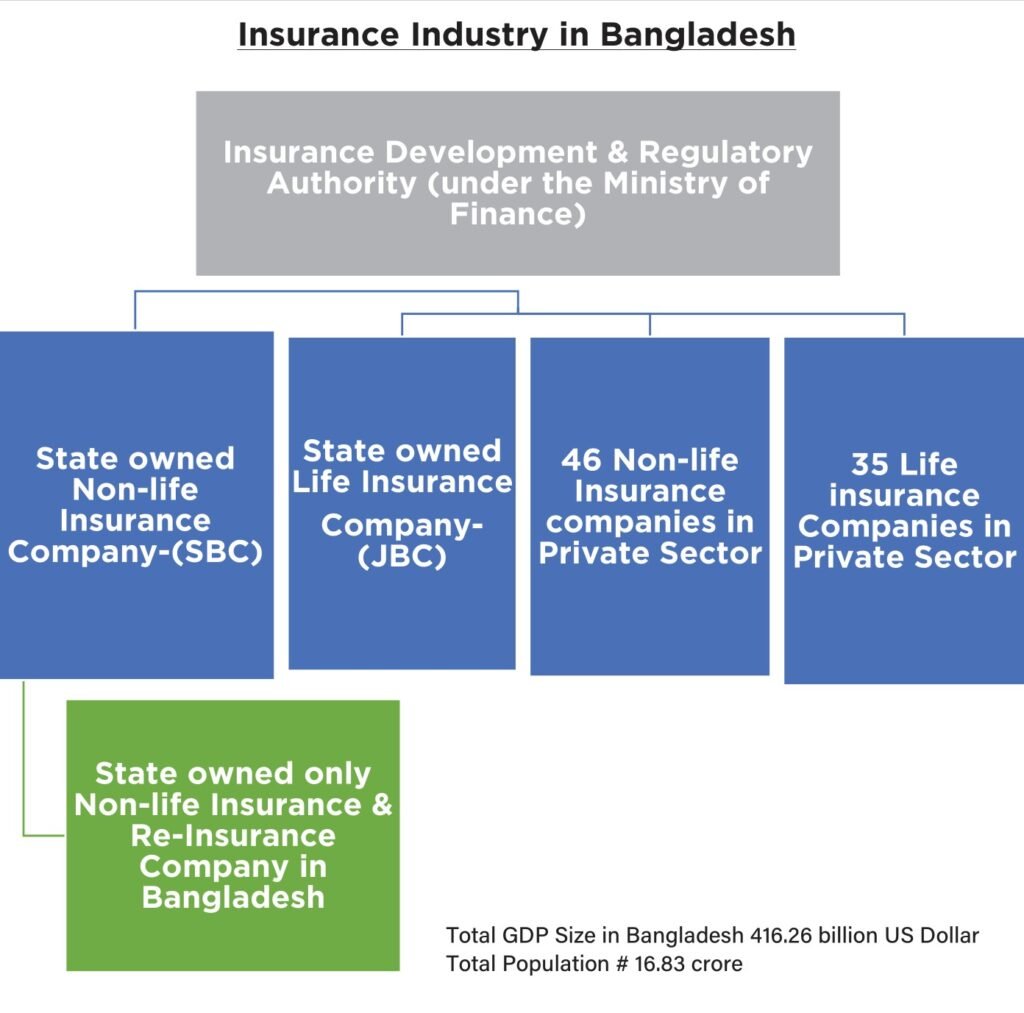

The regulatory framework and role of Insurance Development & Regulatory Authority (IDRA) is fundamental to maintaining stability and promoting growth in Bangladesh’s insurance sector. Established in 2010 under the Insurance Development and Regulatory Authority Act, IDRA replaced the erstwhile Chief Controller of Insurance and assumed comprehensive regulatory powers over the industry.

IDRA’s primary responsibilities include issuing licenses to insurance companies, regulating insurance operations, protecting policyholders’ interests, and ensuring compliance with statutory requirements. The authority monitors solvency margins, premium rates, policy conditions, and investment patterns of insurance companies to maintain market discipline. IDRA also plays a crucial role in developing the insurance market through various initiatives including promoting insurance awareness, facilitating product innovation, and establishing professional standards.

The regulatory body enforces the Insurance Act of 2010, which provides the legal foundation for insurance operations in Bangladesh. This framework mandates minimum capital requirements, corporate governance standards, and financial reporting norms. IDRA’s ongoing efforts to strengthen regulations, improve transparency, and enhance consumer protection mechanisms have been instrumental in building trust and credibility in the insurance sector.

Structure of the Insurance Industry in Bangladesh

The structure of the insurance industry in Bangladesh is characterized by a clear bifurcation between life and non-life insurance businesses. As per regulatory requirements, companies must operate exclusively in either segment and cannot engage in both simultaneously. This separation ensures focused operations and specialized expertise in each domain.

Currently, the industry comprises approximately 35 life insurance companies and 46 non-life insurance companies, though these numbers may vary as the market evolves. The market includes both public sector corporations and private limited companies. On the life insurance side, the state-owned Jiban Bima Corporation holds a significant market share alongside numerous private insurers. In the non-life segment, Sadharan Bima Corporation represents the public sector, competing with a larger number of private general insurance companies.

The industry also includes supporting infrastructure such as insurance brokers, surveyors, and agents who facilitate insurance distribution and claims processing. Reinsurance plays a critical role in risk distribution, with both domestic reinsurance facilities and international reinsurance arrangements supporting the industry’s capacity to underwrite large risks.

Life Insurance Sector in Bangladesh

The life insurance sector in Bangladesh provides financial protection through various products including term insurance, endowment policies, money-back plans, pension schemes, and unit-linked investment products. This segment focuses on long-term financial security, retirement planning, and wealth accumulation for individuals and families.

Jiban Bima Corporation, the state-owned life insurer established in 1973, has historically dominated this sector with its extensive branch network and government backing. However, private life insurance companies have steadily gained market share by offering innovative products, superior customer service, and leveraging modern distribution channels including bancassurance partnerships.

Despite growth potential, the life insurance sector faces challenges in achieving deeper market penetration. Cultural factors, limited financial literacy, and income constraints affect insurance uptake, particularly in rural areas. The sector has responded by developing microinsurance products targeting lower-income segments and expanding agent networks to reach underserved populations. Investment-linked products have gained popularity among urban middle-class customers seeking wealth creation alongside protection.

Non-Life (General) Insurance Sector

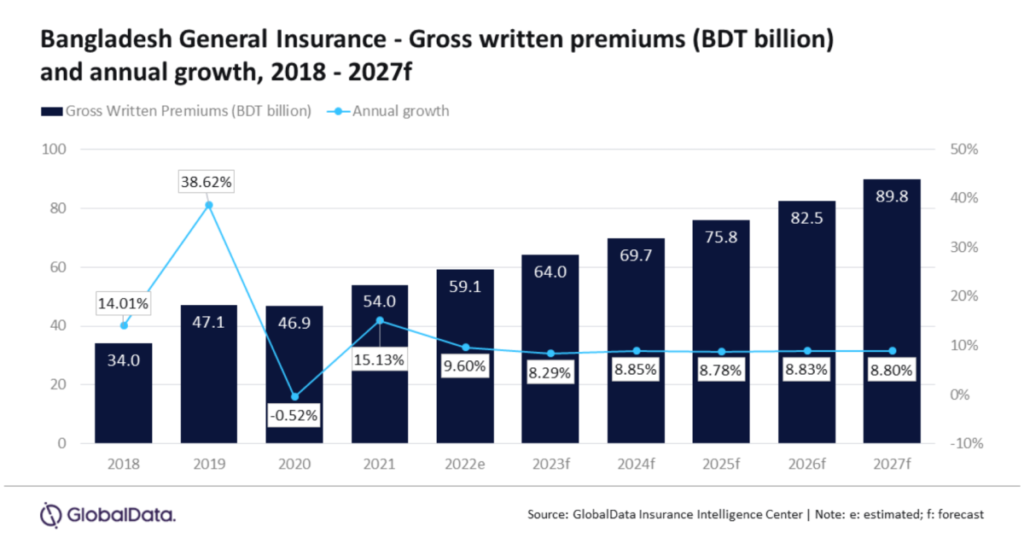

The non-life (general) insurance sector encompasses diverse product lines including fire insurance, marine insurance, motor insurance, health insurance, liability coverage, and other property and casualty insurance. This segment addresses short-term risk protection needs for individuals, businesses, and commercial entities.

Motor insurance represents the largest segment within non-life insurance, driven by mandatory third-party coverage requirements and the country’s growing vehicle population. Fire insurance is another significant product line, particularly for commercial and industrial properties. Marine insurance supports Bangladesh’s export-oriented economy, especially the crucial garment manufacturing sector, by providing cargo and transit coverage.

Sadharan Bima Corporation, the public sector general insurer, competes with numerous private companies in this space. The sector has witnessed increased competition leading to improved service standards and product innovation. However, challenges persist including underpricing of risks, inadequate claims management, and limited penetration in emerging areas like health insurance and cyber insurance. The sector continues to evolve with growing demand for specialized coverages addressing modern risk exposures.

Public vs Private Insurance Companies

The dynamic between public vs private insurance companies shapes Bangladesh’s insurance landscape significantly. Public sector insurers—Jiban Bima Corporation and Sadharan Bima Corporation—enjoy advantages including government support, extensive branch networks, and strong brand recognition built over decades. These entities often dominate certain market segments and benefit from mandatory coverage requirements in government projects.

Private insurance companies bring competitive energy, innovation, and customer-centric approaches to the market. They typically demonstrate greater agility in product development, technology adoption, and service delivery. Many private insurers have introduced contemporary insurance solutions, digital platforms, and efficient claims processing systems that have raised industry standards. Private companies have also been more active in building specialized expertise in niche segments.

Market share distribution has gradually shifted with private insurers collectively gaining ground, particularly in the life insurance segment where product differentiation and service quality matter significantly. Competition between public and private entities has generally benefited consumers through wider product choices and improved service levels. However, concerns about market conduct, financial stability of some players, and need for level playing field continue to be subjects of regulatory attention.

Insurance Penetration and Financial Awareness

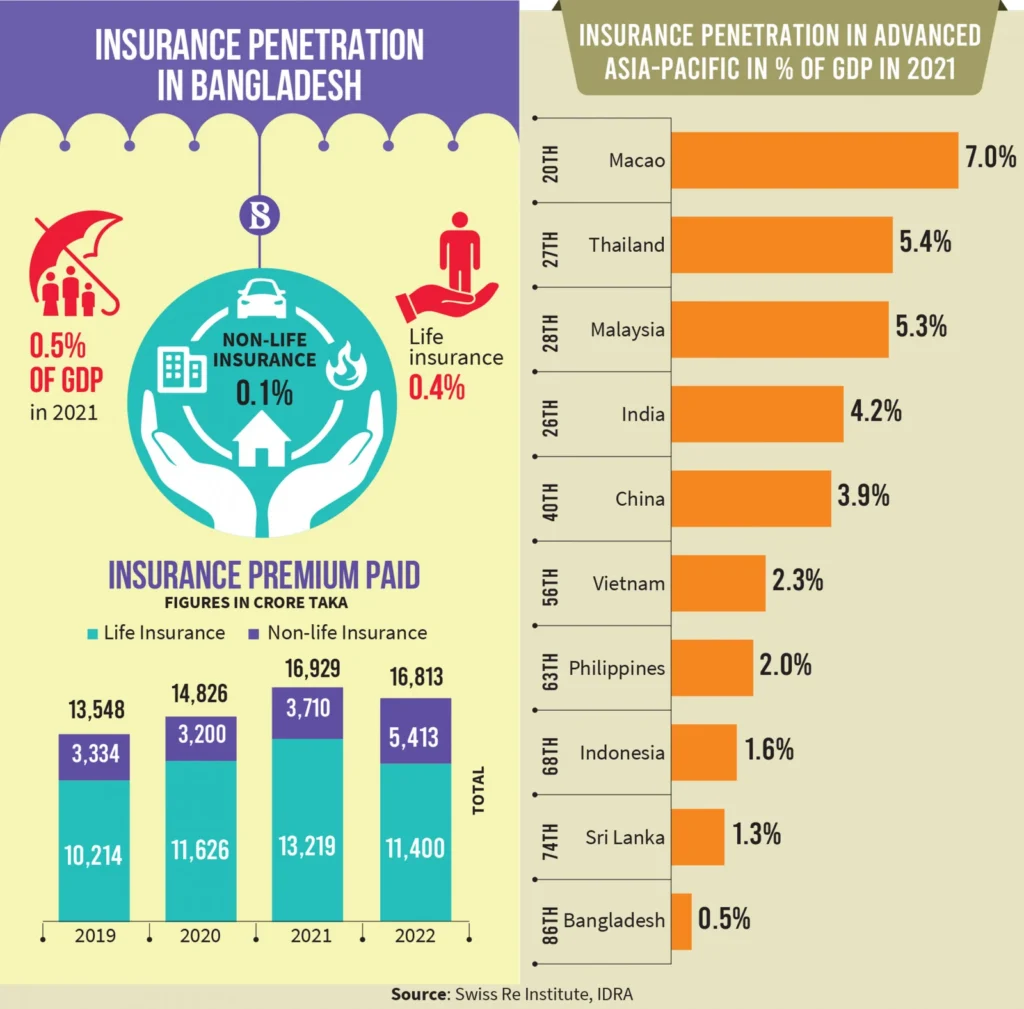

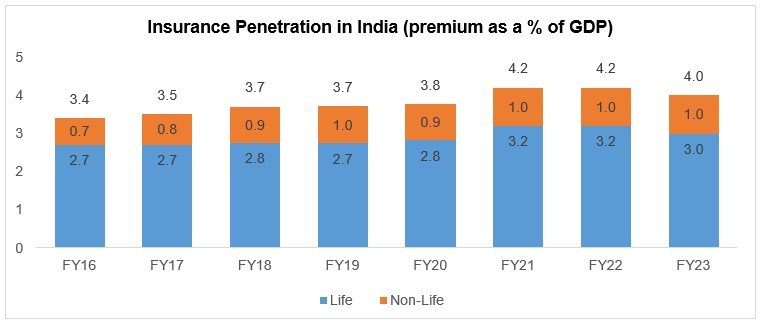

Insurance penetration and financial awareness remain critical challenges for Bangladesh’s insurance industry. Insurance penetration, measured as premium as a percentage of GDP, stands significantly lower in Bangladesh compared to regional and global averages. Current penetration rates hover around 0.5-0.6%, indicating substantial untapped potential in the market.

Several factors contribute to low penetration levels. Limited financial literacy means many citizens lack understanding of insurance concepts, benefits, and product features. In rural areas particularly, traditional saving habits and informal risk-sharing mechanisms compete with formal insurance products. Income levels, while improving, constrain discretionary spending on insurance for large population segments.

Efforts to improve insurance awareness include IDRA-led initiatives, industry campaigns, and financial literacy programs. The introduction of microinsurance products specifically designed for low-income populations represents a strategic approach to expanding coverage. Digital platforms and mobile technology offer promising channels for reaching previously inaccessible customer segments. As economic growth continues and middle-class expansion accelerates, opportunities for increased insurance penetration remain substantial, provided the industry addresses awareness gaps and develops appropriate products.

Insurance Penetration and Financial Awareness

Insurance penetration and financial awareness remain critical challenges for Bangladesh’s insurance industry. Insurance penetration, measured as premium as a percentage of GDP, stands significantly lower in Bangladesh compared to regional and global averages. Current penetration rates hover around 0.5-0.6%, indicating substantial untapped potential in the market.

Several factors contribute to low penetration levels. Limited financial literacy means many citizens lack understanding of insurance concepts, benefits, and product features. In rural areas particularly, traditional saving habits and informal risk-sharing mechanisms compete with formal insurance products. Income levels, while improving, constrain discretionary spending on insurance for large population segments.

Efforts to improve insurance awareness include IDRA-led initiatives, industry campaigns, and financial literacy programs. The introduction of microinsurance products specifically designed for low-income populations represents a strategic approach to expanding coverage. Digital platforms and mobile technology offer promising channels for reaching previously inaccessible customer segments. As economic growth continues and middle-class expansion accelerates, opportunities for increased insurance penetration remain substantial, provided the industry addresses awareness gaps and develops appropriate products.

Challenges Facing Bangladesh's Insurance Industry

Examining the challenges facing Bangladesh’s insurance industry reveals multiple obstacles hindering optimal growth and development. Low insurance penetration remains the most fundamental challenge, limiting the sector’s economic impact and sustainability. Despite a large population, the industry serves only a small fraction of potential customers.

Regulatory and compliance issues present ongoing challenges. Some companies struggle with capital adequacy requirements, while others face governance and transparency concerns. The need for stronger enforcement of regulations and improvement in corporate governance standards remains evident. Claims settlement delays and disputes undermine consumer confidence, making customer acquisition and retention difficult.

Operational challenges include limited professional expertise in underwriting, actuarial science, and risk management. The shortage of skilled insurance professionals affects service quality and product development capabilities. Technology adoption, while improving, remains uneven across the industry. Many companies still rely on paper-based processes and legacy systems that hinder efficiency.

Distribution challenges persist with heavy reliance on traditional agent networks that may lack adequate training and motivation. Product innovation lags behind market needs, with limited availability of specialized coverages for emerging risks. Investment management capabilities need strengthening to generate competitive returns for policyholders while maintaining regulatory compliance. Addressing these multifaceted challenges requires coordinated efforts from regulators, industry participants, and other stakeholders.

Conclusion: Future Prospects of the Insurance Sector in Bangladesh

The future prospects of the insurance sector in Bangladesh appear promising despite existing challenges. The country’s strong economic growth trajectory, expanding middle class, increasing urbanization, and rising awareness of financial planning create favorable conditions for insurance sector expansion. Demographic factors including a large young population present opportunities for long-term growth in life insurance particularly.

Technological transformation offers exciting possibilities for the sector’s evolution. Digital platforms, mobile insurance, artificial intelligence-driven underwriting, and blockchain-based claims processing can revolutionize operations and customer experiences. The growing fintech ecosystem in Bangladesh provides opportunities for innovative distribution models and product designs that could dramatically improve penetration rates.

Regulatory reforms and capacity building initiatives by IDRA will likely continue strengthening the industry’s foundation. Expected improvements in corporate governance, risk-based supervision, and consumer protection frameworks should enhance market credibility. The government’s financial inclusion agenda aligns well with expanding insurance coverage to underserved populations.

Examining Bangladesh’s Insurance Industry reveals a sector at an inflection point, poised for significant growth while navigating substantial challenges. Success will depend on industry participants’ ability to innovate, regulators’ effectiveness in creating enabling frameworks, and collective efforts to build insurance awareness. With strategic focus on technology adoption, product innovation, professional development, and customer-centricity, Bangladesh’s insurance industry can realize its potential as a major contributor to financial stability and economic development. The journey ahead requires patience, investment, and commitment, but the opportunities for transformative growth make this an exciting sector to watch in the coming years.